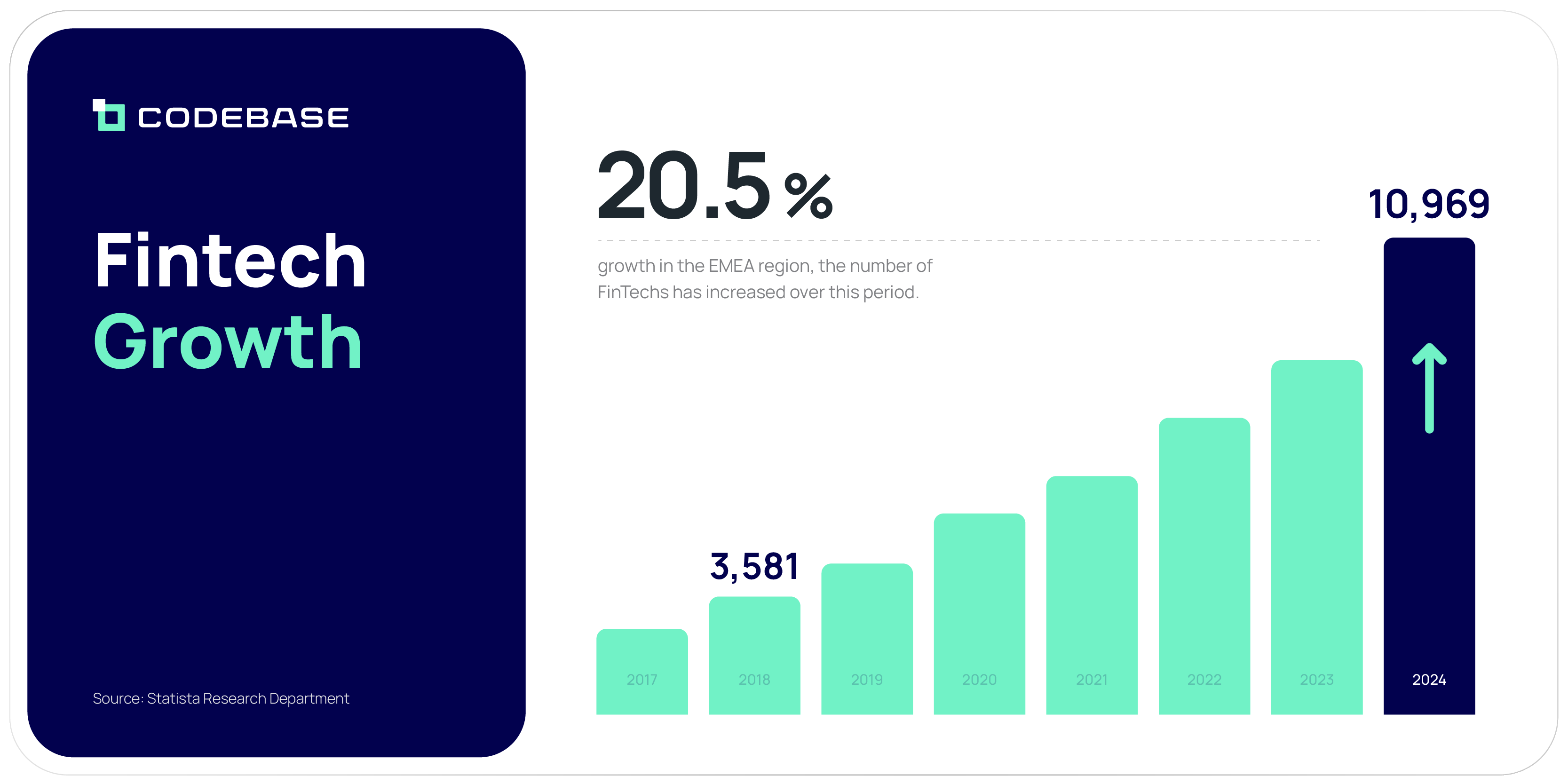

With the rapid advancement of technology, the financial industry is undergoing a major transformation. FinTech, an abbreviation for Financial Technology, is at the forefront of this revolution, reshaping the way we think about and interact with money. This is reflected in the number of FinTech companies across different regions globally. In the EMEA region, for instance, the number of FinTechs has grown from 3,581 in 2018 to 10,969 in 2024, recording a 20.5% growth during this period. This indicates the increasing demand for innovative financial services as technology and market dynamics evolve.

From mobile payments to peer-to-peer lending, FinTech is revolutionizing traditional banking services by providing more convenience, efficiency, and accessibility for consumers. We now have the ability to make instant transactions, manage our personal finances through intuitive apps, and even invest in digital currencies like Bitcoin. As FinTech continues to evolve, it has the potential to disrupt traditional banking models and democratize financial services.

Furthermore, FinTech is not just limited to consumers. It is also transforming the way businesses handle their financial operations, from streamlining payment processing to providing data-driven insights for better decision-making. Entrepreneurs and startups are leveraging FinTech to drive innovation and create new business opportunities.

In this article, we will discuss the key trends and technologies driving the FinTech revolution, as well as the challenges and opportunities that lie ahead.

FinTech Trends and Innovations

The FinTech industry is constantly evolving, with new trends and innovations emerging at a rapid pace. One of the most significant trends in the financial industry is the rise of digital payments and mobile wallets. In the Middle East and Africa (MEA) region, research shows that 85% of consumers used at least one of the emerging payment methods in 2022. This surge can be attributed to the growing smartphone penetration, improved internet access, and a shift toward cashless economies. Companies like Apple Pay, Google Pay, and Samsung Pay have revolutionized the way we make everyday purchases, offering convenient, secure, and seamless payment experiences that delight customers.

Another prominent trend in FinTech is the growth of peer-to-peer (P2P) lending platforms. P2P lending is an alternative lending model that involves connecting borrowers directly with individual lenders through online platforms, bypassing traditional financial institutions such as banks. It allows borrowers to access loans at potentially lower interest rates, while lenders can earn higher returns on their investments compared to traditional savings accounts. This is particularly a game changer for the Small and Medium-sized Enterprises SMEs segment, which has been historically underserved by conventional lending institutions. According to statistics, 88% of SMEs in MENA struggle to access business financing, despite their integral role in economic development and job creation.

Managed Services have also emerged as a key trend in FinTech growth, where financial institutions are delegating their IT and engineering functions to specialized Managed Services Providers (MSPs). This allows financial institutions to focus on their core competencies while benefiting from expertise and advanced support offered by MSPs. Managed Service Providers are responsible for managing the organization's IT infrastructure which involves maintenance, optimization, and ongoing product innovation to enhance business competitiveness.

A typical example of how managed services can streamline operations is BCFC's partnership with Unipal to launch the Unipal Youth Card by IMTIAZ, supported by Codebase. The Managed Services team at Codebase supported BCFC in bringing this initiative to life in just under two weeks, thanks to their extensive understanding of BCFC’s infrastructure as their MSP. The benefits go beyond time efficiency, financial institutions also benefit from lower operating costs, improved service quality, and enhanced scalability.

Blockchain technology is yet another trend that has had a significant impact on the FinTech industry. The decentralized nature of blockchain has enabled the development of cryptocurrencies, such as Bitcoin and Ethereum, which have disrupted traditional financial systems. Blockchain-based applications have also found applications in areas like cross-border payments, supply chain management, and digital identity verification. For instance, statistics show that the use of blockchain could potentially cut transaction costs by up to 80% compared to traditional methods.

Adding to these trends is the rise of embedded finance, which is reshaping how financial services are delivered. Embedded finance refers to the integration of financial services directly into non-financial platforms and applications, allowing businesses to offer banking-like services without requiring customers to leave their environments. For example, e-commerce platforms can provide payment processing, insurance, or lending options at the point of sale, enhancing customer convenience, streamlining the purchase process, and ultimately boosting conversion rates for businesses. Studies have shown that companies that have integrated embedded finance have recorded up to a 30% increase in Average Order Value (AOV) and growth in conversion rates by up to 12%.

As times and technology continue to evolve, the FinTech industry is poised for further innovation and transformation. The benefits of these trends extend across all players—customers, financial institutions, merchants, and FinTech companies. Therefore, all stakeholders must be strategic and intentional in adopting these technologies into their business operations to ensure sustained efficiency in digital finance.

The Role of Blockchain Technology

As we have highlighted, blockchain is one of the key trends today in digital finance. At its core, blockchain technology offers a decentralized and immutable ledger that enhances transparency, security, and efficiency in financial transactions. But what role does it play in shaping the future of FinTech?

- Enhancing Transparency and Trust

One of the most significant roles of blockchain in FinTech is its ability to foster transparency and trust among stakeholders. Each transaction is recorded on a public ledger that is accessible to all participants. This transparency ensures that all parties can verify transactions independently, reducing the likelihood of fraud and enhancing accountability. For financial institutions, this means a more secure environment for conducting business, leading to improved customer trust and confidence.

- Revolutionizing Payment Systems

Traditional payment methods often involve multiple intermediaries, which can slow down the process and increase costs. Blockchain simplifies this by allowing direct peer-to-peer transactions, eliminating the need for intermediaries. Companies like Stellar and Ripple have demonstrated how blockchain can facilitate real-time international payments, significantly reducing transaction times from days to mere seconds while also lowering fees.

- Driving Financial Inclusion

In regions with limited access to traditional banking infrastructure, blockchain-based solutions can offer essential services such as remittances, savings, and loans directly through mobile devices. According to a study by the US Federal Reserve, 5% of adults without a bank account use cryptocurrency to transact, compared to 3% of the banked. This shows how blockchain can bridge the financial gap for underserved communities by providing alternative means of financial participation.

- Smart Contracts for Automation and Efficiency

Smart contracts are self-executing agreements where the terms of the contract directly written into code on the blockchain. In practice, smart contracts can transform various financial operations, such as loan approvals and insurance claims. For instance, in the insurance industry, a smart contract can automatically process a claim and issue a payout when predetermined conditions are met, eliminating the lengthy review processes typically required. This not only accelerates transaction times but also improves customer satisfaction by providing faster, more reliable service.

- Securing Digital Assets

As more financial institutions explore cryptocurrencies and digital tokens, the need for a secure infrastructure has become paramount. Blockchain’s cryptographic principles ensure that digital assets are stored securely, mitigating the risks of hacking and fraud. Moreover, the use of blockchain can provide a clear ownership trail, enhancing the traceability and legitimacy of digital assets.

FinTech and the Rise of Mobile Banking

The ubiquity of smartphones and the increasing reliance on mobile technology have played a critical role in the rise of mobile banking. According to a 2023 GSMA annual report, 54% of the world’s population – equivalent to 4.3 billion people – own smartphones. This trend has been evident in the MENA region, where the smartphone penetration rate is projected to cross 90% by 2030, up from 66% in 2020. This enables consumers to access banking services anytime and anywhere, fostering greater convenience and efficiency in financial transactions.

FinTech companies and innovators are increasingly leveraging this growth to deliver mobile-first solutions that enable customers to manage their finances on the go. This includes mobile banking apps designed to address various consumer needs, such as digital lending, cross-border payments, crowdfunding, investments, personal finance management, and digital wallets.

At Codebase, we have been at the frontline of this transformation, supporting financial institutions across different financial segments to build these solutions for their customers through our Digibanc platform. Some of these products include:

- Digital Wallets – Wink Pay (Lebanon)

Wink Pay, Lebanon’s first mobile digital wallet, offers a complete range of financial services conveniently accessible through smartphones. With features like instant virtual card issuance and digital onboarding via eKYC verification, it provides a secure and seamless digital experience tailored to the needs of Lebanon's population, 55% of whom remain unbanked. Wink Pay addresses this gap by offering easy access to essential financial services.

- Digital Lending – BCFC (Bahrain)

Codebase supported BCFC in building their digital lending mobile app, Sahel, which aims to disrupt Bahrain's $30 billion lending market. Within the first three months of its launch, the app attracted over 20,000 users and enabled BCFC to reduce in-branch card issuance by 50%. Sahel features instant credit decisioning and a seamless digital onboarding process, allowing customers to complete the entire lending process remotely and with ease.

- Crowdfunding – Beban (Bahrain)

Beban Crowdfunding is Bahrain’s first-of-its-kind platform, created to address the business financing and investment gap in Bahrain and the broader GCC region, where 60% of startups face challenges in securing adequate capital. The platform provides investors with an easy and streamlined process to begin supporting startups through their smartphones, offering a much-needed solution to bridge the funding gap for emerging businesses in the region.

- Complete Digital Bank – Ajman Bank (UAE)

Ajman Bank's Super App, built on the Digibanc platform, is a fully mobile-first digital banking solution. The app allows customers to access a full range of banking services, including account management, payments, loans, and credit cards, all through an intuitive mobile interface. With its cloud-based infrastructure hosted on Microsoft Azure, the app enables seamless scalability and security, while allowing customers to conduct banking transactions wherever they are.

Smartphone penetration has opened up new opportunities for financial institutions to reach customers, particularly in developing countries where access to traditional banking services may be limited. It’s inspiring how FinTechs, financial institutions, governments, and other players are increasingly collaborating to offer a level of convenience and accessibility that was previously unimaginable.

Advantages of FinTech in Financial Services

The growth of FinTech has brought about a significant transformation in the financial industry that benefits consumers, businesses, and financial institutions alike. Some of the key benefits for consumers include:

- Speed and Efficiency

Traditional banking often involves lengthy procedures that can frustrate customers and lead to delays. In contrast, FinTech solutions offer instantaneous experiences, allowing for rapid fund transfers, swift loan approvals, immediate access to account information, etc. This enhanced speed not only improves customer satisfaction but also enables businesses to operate more efficiently and respond quickly to market demands.

- Personalization of Experiences

The demand for personalized financial services is rising. Research indicates that a significant percentage of banking consumers – 70% – consider personalization to be a critical factor in their banking experiences. FinTech companies harness data analytics to tailor products and services to individual customer preferences, ensuring that users receive relevant offerings that meet their unique needs.

- Affordability of Banking Services

FinTech is reshaping consumer expectations regarding the cost of banking services. According to the World Retail Banking Report 2022 by Capgemini and Efma, a notable 75% of surveyed customers are drawn to the cost-effective and seamless solutions provided by FinTech firms. This trend is pushing traditional banks to reevaluate their pricing structures and enhance their service offerings to remain competitive. As a result, consumers benefit from lower fees and improved access to financial services.

- Financial Literacy and Empowerment

FinTech is playing a significant role in accelerating financial literacy in both developing and developed countries. This is achieved through various digital platforms and tools that provide accessible resources, such as budgeting apps, webinars, podcasts, and other educational content, which have become increasingly available in the modern age of FinTech.

- Increased Accessibility of Financial Services

FinTech has significantly improved access to financial services, particularly in underserved regions where access to traditional banks is limited. FinTech solutions, such as mobile apps, allow customers to access a full range of banking services from the comfort of their homes, breaking down the geographical barriers that have traditionally hindered access to banking services.

Regulations and Challenges

As the digital financial industry continues to evolve and disrupt traditional financial services, it has also faced a unique set of regulatory and compliance challenges. Financial services have historically been one of the most heavily regulated industries, and FinTech companies must navigate a complex web of rules and regulations to operate effectively.

One of the primary challenges for FinTech firms is the need to comply with various financial regulations, such as anti-money laundering (AML) laws, know-your-customer (KYC) requirements, and data privacy regulations. These compliance requirements can be particularly burdensome for smaller FinTech startups, which may lack the resources and expertise to navigate the regulatory landscape effectively.

Additionally, the rapid pace of innovation in the FinTech industry has outpaced the ability of regulatory bodies to keep up. Policymakers and regulators have struggled to strike a balance between fostering innovation and ensuring the stability and security of the financial system. This has led to a patchwork of regulations across different jurisdictions, creating uncertainty and compliance challenges for FinTech companies operating in multiple markets.